On 28 May 1962 the Dow Jones average of thirty leading industrial stocks dropped by 34.95 points. At the time this was a drop bigger than on any other day in history, with the exception of the crash on 28 October 1928.

On Tuesday 29 May 1962 the market suddenly changed direction with the index gaining 27.03 points by the close of day.

Wednesday was a public holiday, but Thursday saw the index climb another 9.4 points, leaving it slightly above where it was before all the excitement had begun.(Source: Business Adventures, John Brooks)

At that time, President Kennedy’s retrospective analysis eluded to the steel industry’s planned price increase. However, he couldn’t have been more wrong.

Back to Monday, 28 May 1962, when brokers used teleprinters to distribute updates. The massive sell-off caused a delay of up to 52 minutes between trading volumes and teleprinting the prices. Since the machine could no longer keep up with new information, it consistently showed lower prices, inconsistent with trading volumes. This in turn caused mass hysteria and panic among investors.

By lunchtime, brokers all over Wall Street had to deal with a flood of walk-in clients trying to sell their shares. Eventually radio and television stations got wind of a rapidly “falling” market, resulting in even further sell-offs. The story did not end in Wall Street, however. News filtering through to the rest of the world led to even further sell-off in Europe, dropping copper prices, missed margin calls, et cetera.

By Tuesday morning the calculated loss in value in the stock market amounted to $20,800,000,000 – a record at the time which even surpassed the height of the 1929 crash. As mentioned above, the market eventually corrected itself and was back to normal by Thursday that week.

Human sentiment, fear, and emotions were the drivers of one of the craziest weeks in stock market history.

Moving forward to the present: what we are witnessing in current markets has a slightly similar feel, as the world tries to wrap its head around the impact of the Covid-19 pandemic.

At this stage it is almost impossible to determine the long- term effect that the virus will have on the world economy. It might be naïve, however, to declare that “this is the beginning of the end”, given how similar situations in the past such as SARS, Ebola and Swine Flu, came and went without much long-lasting repercussions on the world economy.

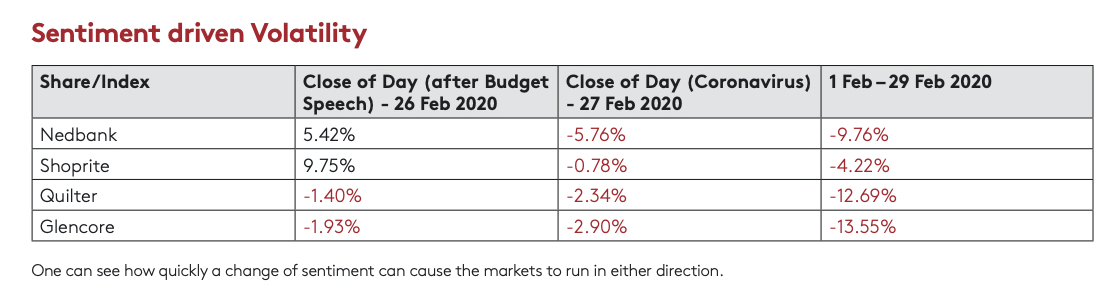

Further on sentiment-driven markets, it is worth noting that Tito Mboweni (Finance Minister of South Africa) recently presented his 2020/2021 budget speech, outlining plans to stabilise an increasing debt burden. Many thought it was an impossible task but Mboweni managed to surprise markets by suggesting reductions in the public sector wage bill.

Not many could have predicted such a bold move and as a result we witnessed an almost immediate rise in the share prices of a number of the reputable listed South African companies (companies that derive most of their earning from South African operations), and a decline in the stock of those JSE-listed companies that derive most of their earnings offshore – because in their case the focus remained on Covid-19.

Of course, the very next day (27 February 2020), positive sentiment about South Africa was overpowered by further fears surrounding Covid-19, and we saw downward price pressure across the board.

To illustrate our point, see the table above where Nedbank and Shoprite are the South African incorporated companies, and Quilter and Glencore are offshore companies. All four shares trade on the same exchange, but sentiment drove the price in very different directions. Column 4 illustrates the effect of volatility for the month of February 2020.

In conclusion, we refer to an earlier article written by Rene Olivier, MD of Wealth at IJG, highlighting the impact of such volatility and how to handle it.

“Constructing a portfolio around binary outcomes will result in you chasing your tail and paying brokers unnecessary trading fees. How easy was it to predict that Trump would be president of the biggest economy in the world, or that Ramaphosa would become president of South Africa”? Or now, to predict

Covid-19? “These things are often not that important to predict. What is important is that you understand what you want to achieve (broken down into tangible objectives) and decide what investment solutions will match your objective’s time horizon. Thereafter, you can sit through volatility and protect the permanent loss of capital as you compound over your investment horizon by being adequately diversified and always paying the right price”.