2022 Overview

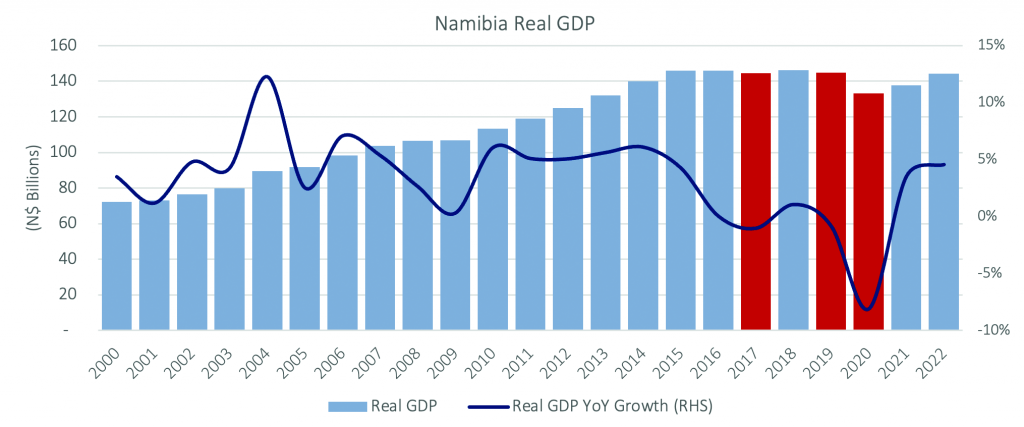

The Namibia Statistics Agency’s (“NSA”) Preliminary National Accounts data shows that the Namibian economy recorded real GDP growth of 4.6% in 2022, the quickest since 2014. Negative growth in 2019, followed by the sharp downturn in 2020 of 8.1%, meant that the relatively quicker economic growth Namibia experienced in 2021 and 2022 was from a low base, and overall output remained below the peak of 2018.

As was the case in 2021, the growth in 2022 was primarily driven by growth in mining output, with the sector posting growth of 21.6%. Growth within the sector was in large part due to increased diamond production following the commissioning of Debmarine’s Benguela Gem mining vessel. The uranium mining sub-sector recorded a moderate contraction in 2022, following a strong increase in the value of uranium exported in 2021. Namibia was the world’s third-largest (3rd) uranium producer in 2022 and accounted for 11% of global production. The Agriculture, Forestry and Fishing sector recorded moderate growth of 2.6%.

Growth from the secondary industries was mixed, with Manufacturing output climbing by 5.0%, Electricity and Water growing by 10.3%, and construction contracting by 16.4%, making it the seventh (7th) consecutive year the sector has recorded negative growth. In real terms, the sector’s output in 2022 was 25% of that of 2015. The Manufacturing sector’s growth was mainly attributed to robust growth in the diamond processing sub-sector.

The tertiary industries again posted moderate growth in 2022 of 2.2%. Wholesale and Retail Trade, often seen as a proxy of consumer sentiment, encouragingly logged growth for a second (2nd) consecutive year of 6.0%. Output for the sub-sector was however still well below the highs of 2016. Nonetheless, the growth suggests broader economic drivers beyond just mining, and that consumer sentiment is improving on a somewhat sustained basis. The NSA reported further growth for the sub-sector in Q1 2023, which means that the sub-sector is on track to surpass the output levels of 2019. The Hotels and Restaurants sub-sector saw a similar recovery during 2022 on the back of an increase in tourist activity. Following a contraction in 2021, Financial and Insurance Services recorded moderate growth as banks benefited from margin expansion, although output remained below 2020 levels.

Information Communication’s output grew by 2.5%, materially slower than the growth recorded in 2021, as people returned to work, resulting in increased face-to-face engagement and fewer mobile minutes being used. Healthcare Services logged strong growth of 8.0% attributed to increased health personnel capacity. Public Administration and Defence, or government output ex-health and education, which was relatively flat in 2021, recorded a 0.9% contraction in 2022 as fiscal consolidation measures and the hiring freeze remained in place.

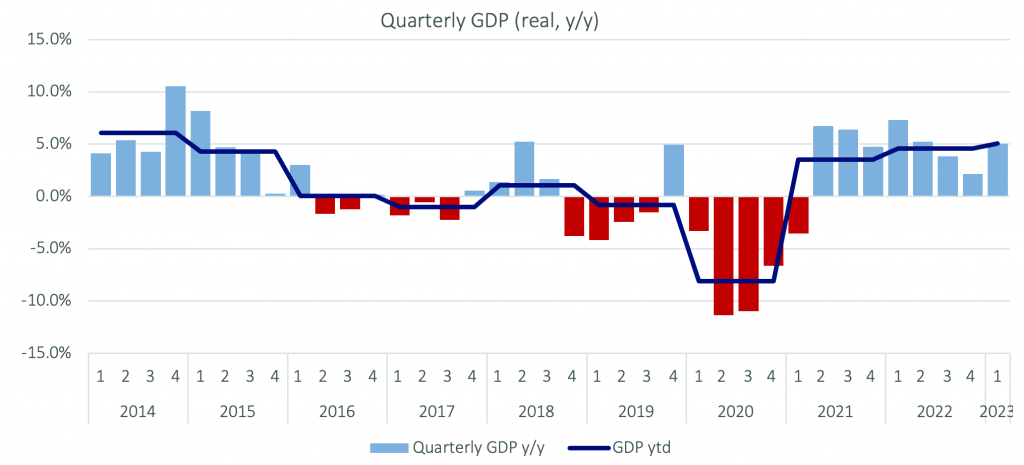

Despite the 4.6% growth in 2022, GDP remains below the high-water mark level of 2018. 2022 output levels were just below the pre-pandemic levels of 2019, meaning that the economy has now more or less recovered from the effects of the extreme lockdown measures implemented by the Government. Namibia has now encouragingly recorded eight (8) consecutive quarters of year-on-year growth, with five (5) of these quarters registering growth of 5.0% and higher.

Outlook 2023

Global Macro

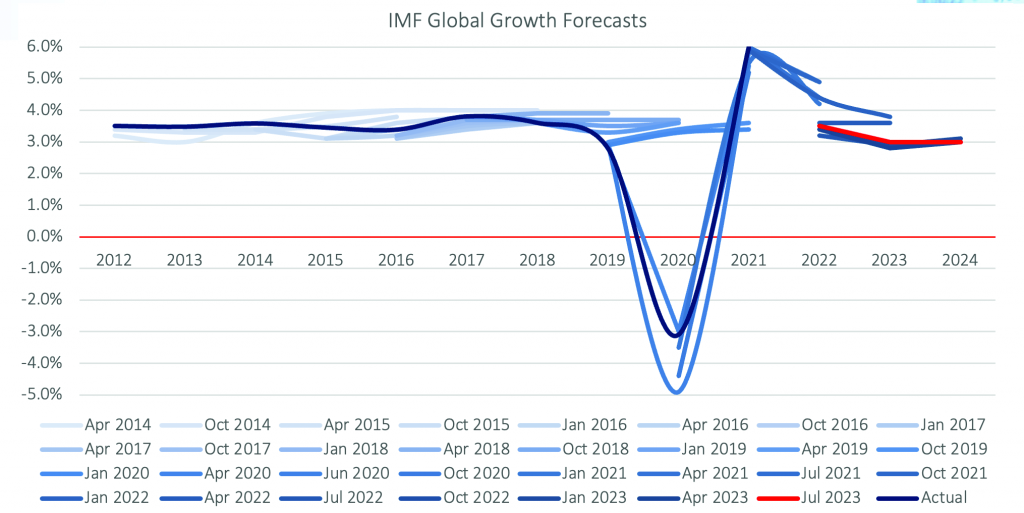

The majority of the global macroeconomic outlook themes of 2022 have spilt over to 2023. Most economic debates are still focused on whether the US will be entering a recession this year, how many more rate hikes we will see from central banks around the world to tame inflation, and the continued impact of the Russia-Ukraine conflict on the world economy. The International Monetary Fund (“IMF”) raised its global GDP growth forecast for 2023 to 3.0% in July. While this is slower than the 3.5% growth recorded in 2022, it is faster than the 2.8% projection of April. The global growth forecast for 2024 was left unchanged at 3.0%.

One of the most widely forecasted US recessions in history has yet to make its landfall. The US economy has shown remarkable resilience over the last two (2) years, in the face of elevated inflation, aggressive rate hikes by the Federal Reserve, the debt ceiling standoff and the banking sector turmoil. The IMF has revised its 2023 growth forecast for the US upwards by 0.2 percentage points to 1.8%, on account of robust consumption growth which reflects the strength of the labour market. This however does not mean that the US is completely out of the woods yet, as excess savings built up during the pandemic are declining, and monetary tightening could tip the economy into a recession. However, high frequency data that keeps surprising to the upside suggests that there might be a wider path to the elusive “soft landing” than initially predicted, in which inflation is tamed without a sharp rise in unemployment. Either way, if the US does enter a recession this year, or in 2024, it will likely not be as severe as some initially feared. It is thus improbable that we will see a US recession triggering a ‘risk-off’ sentiment as severe as we witnessed during the Covid-19 pandemic, which resulted in domestic bond yields spiking and sudden, material local currency depreciation.

At present, a more significant concern arises from the ongoing war in Ukraine, as the conflict appears to be far from over. The most immediate risk is that geopolitical tensions intensify and that the world economy separates into blocs, resulting in more trade restrictions, and a rebound in energy and food prices. Russia has been cosying up to African nations, and at a Russia-Africa summit in July promised free grain supplies to six African countries, following the country’s decision to pull out of the grain deal that was brokered by Turkey in 2022. The deal, which lasted about a year, allowed billions of US dollars worth of grain to safely transit out of Ukraine via the Black Sea. Wheat prices have been climbing globally since Russia withdrew, which places further upward pressure on food prices.

Domestic Growth Forecast

Current forecasts are for the Namibian economy to grow by around 3.0% in real terms in 2023 and 2.9% in 2024, according to the Bank of Namibia (“BoN”). This will result in output levels surpassing their 2018 peak levels for the first time. Primary industries are projected to grow by 5.2% in 2023, following the robust growth recorded in 2021 and 2022. The mining sector, and particularly the diamond mining sub-sector, is anticipated to continue supporting overall GDP growth in 2023, albeit at a slower pace than the last two years. The ongoing oil exploration and appraisal activities should also contribute to the mining sector’s growth in 2023.

Secondary industries are forecasted to grow by 3.2% in 2023, on the back of improved growth rates for the manufacturing, as well as the electricity and water sector. The construction sector is, however, projected to experience further contractions. The tertiary industries meanwhile are forecasted to grow by a relatively subdued 2.1% in 2023.

Domestic inflation

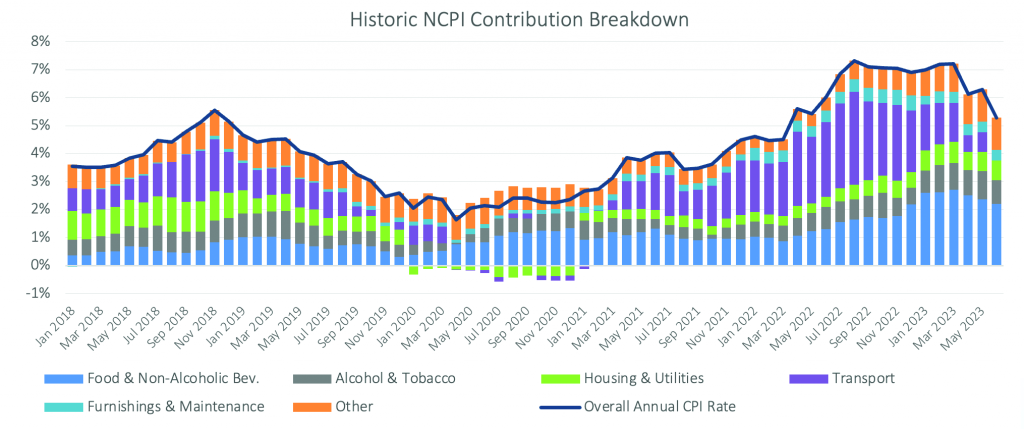

Similar to the global trend, the Namibian Consumer Price Inflation (“NCPI”) rate peaked during the latter half of 2022, reaching 7.3% in August. The NCPI rate has been dropping steadily since April 2023, with June’s 5.3% print the lowest in a little over a year. Namibian inflation remains influenced by supply-side factors, evidenced by goods inflation, which is currently running at almost twice the rate (6.5% y/y in June 2023), in contrast to services inflation at 3.4% y/y.

The ‘transport’ category (depicted in purple in the chart below), which has consistently been the largest driver of inflation in the country between September 2021 and December 2022, is now no longer contributing to the annual NCPI rate, as fuel prices are now 7.0% lower than they were a year ago. Food inflation, while slowing, remains elevated at 11.7% y/y. ‘Housing and Utilities’, which has the heaviest weighting in the inflation basket at 28.4%, is posting relatively moderate inflation of 2.8% y/y, primarily due to increases in rental prices being muted at 2.1%.

Going forward, we expect the disinflationary trend to continue over the short term, although at a moderating pace. IJG’s inflation model is currently forecasting that the NCPI rate will end 2023 between 4.1% and 5.1%, and slow to around 4.2% in 2024. Inflationary risks however remain to the upside, as a recovery in oil prices is possible, especially if OPEC+ continues to cut supply or if economic activity picks up more than expected. Other risks include the potential impact of El Niño on agricultural output, resulting in higher food prices (more on this later). Moreover, an escalation in geopolitical tensions could lead to increased commodity prices and supply constraints, ultimately resulting in higher overall prices.

Interest Rates

Central banks’ fight against inflation continued in 2023 as several have raised borrowing rates to the highest levels in at least two decades. Inflation is easing in most countries but remains relatively elevated, and well above target levels, prompting central banks to keep monetary conditions restrictive. The Federal Reserve Bank’s Chairman, Jerome Powell, noted at the July Federal Open Market Committee meeting that the central bank will be assessing “the totality of the incoming [economic] data” as well as the implications for economic activity and inflation. There is widespread consensus that the Fed is either done hiking rates or at least very close to done.

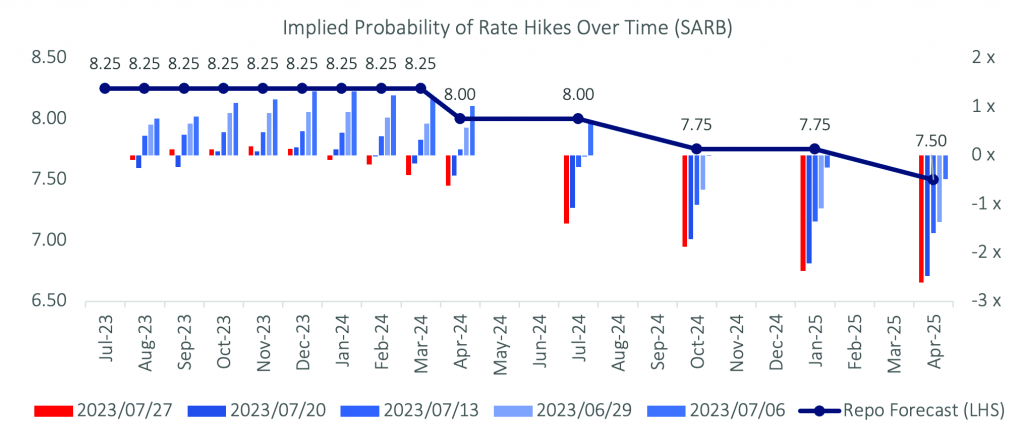

Closer to home, the South African Reserve Bank’s (“SARB”) Monetary Policy Committee (“MPC”) surprised the market in July by holding borrowing rates steady for the first time since November 2021, ending a rate hiking streak of a cumulative 475bps at 10 consecutive MPC meetings. The SARB however stopped short of claiming victory in its fight against inflation, holding the door open for further increases. Going forward, decisions will very much be data driven. The current pricing of the Forward Rate Agreement (“FRA”) curve suggests that the SARB has completed its rate-hiking cycle, at least for the time being, and that the central bank will start cutting rates sometime during Q2 2024.

After deviating somewhat from the SARB in both November 2022 and April 2023, by announcing rate hikes that were 25bps smaller than the SARB’s, the BoN decided to act in kind at the June MPC meeting. The governor stated that the relatively wide spread between SA’s rates and Namibia’s were “creating challenges”. He noted that the BoN had seen outflows of N$10.1 billion to South Africa during the first five (5) months of 2023, and added that “what we need to do now is to close the gap before it becomes a bigger problem.”

The Governor’s comments showed that the central bank is somewhat caught between a rock and a hard place at present. The domestic inflation rate has been ticking down meaningfully since March, meaning that there is little reason to hike rates further at this point. However, should the SARB wish to continue protecting the value of the Rand by hiking rates further over the coming months to ‘stay ahead’ of more developed nations, the BoN will have little choice but to follow suit, despite it hurting indebted consumers and businesses at a time that it is not necessarily needed.

Fiscus and the Budget

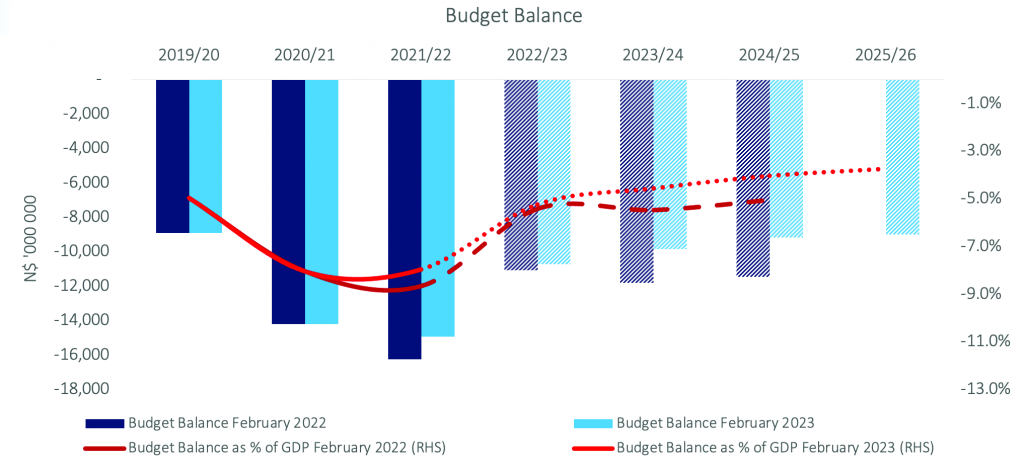

In February, we saw the Minister of Finance and Public Enterprises deliver one of the most positive sounding budgets we have seen in the last decade. The Government’s fiscal position is expected to improve further in 2023/24, with the Ministry projecting to receive N$74.74bn and to spend N$84.58bn. The forecasted revenue figure was revised upwards by N$5.83bn or 8.5% after already being revised upwards by 11.5% in the mid-year budget in October. The projected expenditure for 2023/24 was revised upwards by N$6.56bn or 8.4% from the mid-year budget. The annualised growth rate in budget expenditure since 2019/20, or the last pre-Covid year, is a somewhat reasonable 5.9%, slightly lower than the 6.4% growth in revenue over the same period.

2023/24 will see the smallest absolute deficit in four (4) years. This will also be the first budget deficit of less than 5.0% in more than a decade. The funding requirement for 2023/24 amounts to N$10.08bn, significantly lower than the N$19.38bn requirement of 2022/23 and N$30.40bn for 2021/22. The borrowing requirement will be roughly in line with debt service costs of N$10.02bn in 2023/24, meaning that all debt issued will effectively cover interest costs only, whereas in prior years debt funded other expenditure as well. Thus 2023/24 will be the first primary budget (excluding interest and other statutory costs) surplus in quite some time. Total debt as a percentage of GDP is expected to peak at 70.5% in 2024/25, falling thereafter. Total Government debt is expected to reach N$150.87bn in 2023/24, N$160.02bn in 2024/25 and N$166.22bn in 2025/26.

We feel it would be prudent to remain somewhat sceptical regarding some of the specific revenue drivers for the Medium-Term Expenditure Framework (MTEF) period. SACU revenues have long been unpredictable, or at least inconsistent, and the projections are for very healthy SACU revenues, although decreasing modestly, in the outer MTEF years. Our view is that the future of SACU revenues is quite uncertain, and we would have preferred to see some additional caution applied to these projections. Similarly, the elevated rate of growth projected in company taxes suggests a resurgence in business confidence which is not yet broadly visible in our opinion.

Energy – Green Hydrogen and Oil

Much of the longer-term growth optimism continues to be placed on Namibia’s green hydrogen ambitions, particularly by the Government, and the recent oil finds. Two more deep-water oil discoveries were made by Shell in 2023 at its Jonker and La Rona exploration wells, following the two discoveries made by TotalEnergies and Shell in 2022. Initial estimates by Wood Mackenzie are that the country’s oil resources are around 11 billion barrels of oil equivalent along with 2.2 trillion cubic feet of natural gas reserves. It should be stressed at this stage that it is still very early days on both the oil and green hydrogen fronts and that any potential oil revenues will only start flowing at the earliest in 2028. Still, the fact that TotalEnergies is ploughing half of its 2023 global exploration budget into its exploration and appraisal drilling operations in Namibia is certainly sending out promising signals.

We noted last year, that in the near term, the discoveries are likely to impact Government budget ceilings and allocations as certainty regarding the viability of exploiting the resource improves. With the possibility of substantial future windfall revenues, the Government may experience reduced pressure to limit debt issuance. Consequently, as confidence grows regarding the feasibility of oil extraction, the Government might resume taking on an expansionary role in the economy.

On the green hydrogen front, the Government is continuing in its quest to position Namibia as a major producer towards the latter part of the decade. However, at present the process of generating hydrogen from low-carbon energy sources remains costly, making it less competitive in comparison to hydrogen produced from fossil fuels. To rival grey hydrogen and fossil fuels, green hydrogen heavily relies on foreign government incentives and strategic interventions. We, therefore, remain somewhat sceptical of Namibia’s green hydrogen ambitions for now, especially as it is still early days and global competition in this space seems high.

Potential Headwinds

While the longer-term economic outlook seems positive, short-term risks persist. There is a generally held view that Southern Africa will possibly transition into an El Niño state in the 2023/24 summer season. Such a system typically leads to increased summer temperatures and lower rainfall, which adversely affects dam levels and crop production. Namibia did not have a particularly great rainy season in 2023, and below-average rainfall in 2024 will see stricter water restrictions imposed by NamWater, which will hamper economic activity. The intensity and duration of an El Niño state however remains uncertain at present.

Another risk Namibia continues to face is its energy supply. The well-documented struggles by South Africa’s Eskom led to the power utility cutting its supply contract with Namibia by half to 100MW. NamPower has mostly been able to make up for this by importing more electricity from the Southern African Power Pool, however, Zambia has already threatened to curb exports from its hydropower plants in anticipation of electricity shortages stemming from the El Niño weather phenomenon. This will undoubtedly put further pressure on Namibia’s electricity supply.

Lastly, while the domestic fiscal outlook for the next few years is positive, it is very reliant on SACU revenues being higher over the MTEF period. As mentioned in the Fiscus section, these are typically unpredictable and inconsistent, and the fiscal situation could easily deteriorate if these revenues do not come through as predicted by the Government. This will lead to higher deficits and borrowing costs than forecasted.

Eric van Zyl | Managing Director Designate

Danie van Wyk | Sales and Research