About the author: Ekkehard Friedrich is a Partner at Eos Capital, Namibia’s premier private equity fund management firm and an active supporter of developing Namibia’s Green Hydrogen future.

The Namibian government has done a sterling job at positioning Namibia as a premier producer of Green Hydrogen and Ammonia, and has recently accepted nine bids for developing the opportunity further, putting our country firmly on the radar for large scale international investors in the sector.

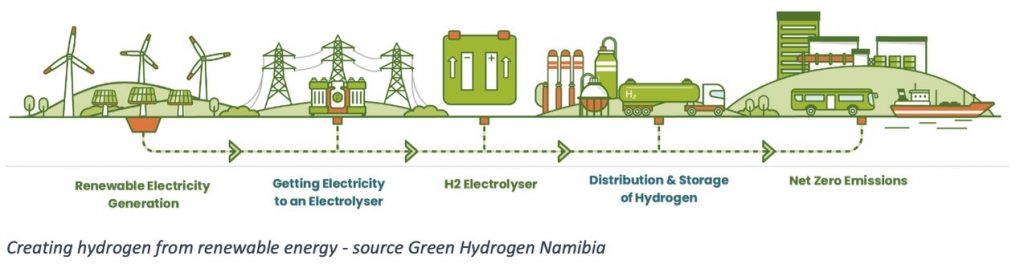

Green hydrogen is hydrogen produced entirely from renewable resources and when combusted only emits water vapour (2 H2 + O2 → 2 H2O). It is therefore deemed as one of the cleanest sources of energy. Green ammonia can easily be produced from green hydrogen (N2 + 3H2 → 2NH3) and has the advantage that it is easier to transport in its liquid state. It can also be mixed with other fuels and burned by existing engines such as ship engines, be used in chemical processes or as a sustainable fertilizer in large scale agriculture.

Much has been said about the green hydrogen opportunity for Namibia by proponents and sceptics alike as it is hard to comprehend its sheer size and with parts of the technology solution yet to reach maturity.

To illustrate the magnitude of this initiative, consider that Namibia currently has an effective installed generation capacity of roughly 500 Megawatt (not all of which is constantly available or utilized) with a peak demand of more than 600 Megawatt, which is widely supplemented by imports from the Southern African Power Pool “SAPP”. The green hydrogen bids propose installing 1 and 5 Gigawatts of renewable energy capacity to produce between 100 to 500 kilotonnes of green hydrogen per year – this is up to one hundred times more than what is currently installed in country!

Reduction of emissions from non-renewable sources of fuel in the European Union:

- In 2021, the EU adopted legislation that aims to reach net zero green house gas emissions by 2050, and as an interim target, by 2030 reduce emissions by 55% below 1990 levels;

- One of the targets, called ‘Fit for 55’, is for renewable energy to account for 40% of final consumption in 2030, up from 20% in 2019;

- This is to be cascaded down to individual country level, as for example, the UK is mandating that all coal-fired power plants come offline by the end of October 2024, with the last closure set for September 2024;

- One instrument used is the introduction of punitive carbon taxes that ratchet up leading to 2050 – currently Sweden leading at a whopping EUR 100 per ton of emissions!

- This led large industrial players such as Thyssen Krupp that traditionally operated on gas, oil or coal to now already transitioning their plants to hydrogen, marking a path of no return;

- Even mining houses such as Anglo American are piloting using hydrogen to power gigantic ore haul trucks

Mounting pressure to end nuclear power and long development lead times:

- 27% of the EU power mix still stems from nuclear sources which is not favoured due to inherent safety risks and nuclear waste disposal issues;

- Germany has vowed to switch off their last nuclear plants with a total capacity of 8.5 Gigawatt by 2022;

- The UK generates about 20% of its electricity from nuclear, but almost half of current capacity is to be retired (4.7 Gigawatt) by 2025. One new generation plant called Hinkley (3.2 Gigawatt) will come on stream soon, but the lead time for developing more of these newer and safer plants takes decades;

- This leaves an electricity generation gap of 10 Gigawatt by 2025 from these two countries alone which may lead to a short term extension, but opens a very attractive window of opportunity for finding an accelerated route to market for a more sustainable source of energy.

Current intermittent renewable sources such as wind and solar cannot fill the gap, with hydrogen emerging as one of the few viable alternatives that is receiving substantial attention and funding:

- As mentioned above, nuclear is typically not seen as a green or renewable generation source;

- European countries are grappling with the limitations of solar and wind energy due to its intermittent nature and require base load capable alternatives to reach climate targets;

- The EU is targeting to construct 5 Gigawatt of green hydrogen generation capacity;

- Germany has allocated EUR 7 billion for developing green hydrogen sources and EUR 2 million for international partnerships in 2021 alone, with funding from the EU projected to be around EUR 400 billion over the next ten years.

While the case for the demand for green hydrogen seems to be well made, the question that begs to be answered is why Namibia is so prominently featuring in attracting international investors to produce green hydrogen.

The answer lies in the production cost and the quality of renewable resources. According to a study undertaken by the Port of Rotterdam in 2021, the area around Lüderitz in Southern Namibia is rated as the third-best site in the world with a projected capacity factor of 77% due to the combination of extremely attractive wind and solar irradiation profiles, which is almost unheard in the world of renewable energy – solar alone would yield a capacity factor of merely 30-35%.

The quality and cost of the renewable resource and land directly translates into the cost of green hydrogen that can be produced from such a resource. McKinsey and Company projects that green hydrogen could be produced at a cost of USD1.50 per kilogram in Namibia and landed in Europe at a price as low as USD2.9 per kilogram after accounting for the cost of desalinating water, converting hydrogen to a transportable state, shipping and converting back to a usable state. This is 10.3% lower than what is deemed possible for the closest competitor (Saudi Arabia) and therefore presently the most attractive solution for European off takers – in the world.

Due to the relative unattractiveness of the European renewable resources, countries such as Germany have realized that green hydrogen cannot be economically produced in the EU and has to be sourced from countries such as Namibia, where it can be produced economically at source and then imported. In fact, Germany has already signed partnership agreements with countries like Namibia and Australia where favourable wind and solar irradiation and wind profiles exist, in a race to secure green hydrogen supply for its economy in the light of its policy drivers mentioned earlier.

Once Namibia has secured the investors and developers for this mammoth project, the benefits for the local economy are unimaginable. Exports of green hydrogen, possibly in the form of ammonia for easier shipping, as well as the possible export of excess electricity, will boost Namibia’s balance of payments which was historically strained by being a net importer of goods and services. Bulk desalinated water required for the hydrolysis process and ammonia will be widely and cheaply available which can be used to support substantial industrial and agricultural developments. Bulk cheap electricity sold into our national grid or consumed at source could greatly improve the nation’s competitiveness and lead to localizing heavy industry which would, in turn, boost job creation.

This project really has the potential to properly “move the needle” for Namibia and there is a very realistic chance that it will take off in the country given the demand and the international drive for decarbonizing, Namibia’s competitive advantage in terms of quality of renewable resources, political stability, and last but not least being one of the first movers in this space.

We commend our government and all stakeholders involved for navigating these uncharted waters to afford our country access to this “once in a lifetime” opportunity and give it our continued and wholehearted support.